Tag: Crane Bank Ltd

DFCU Bank Attorney’s to Rajiv Ruparelia: “Re: Notice Before Legal Action” (05.10.2018)

Share this:

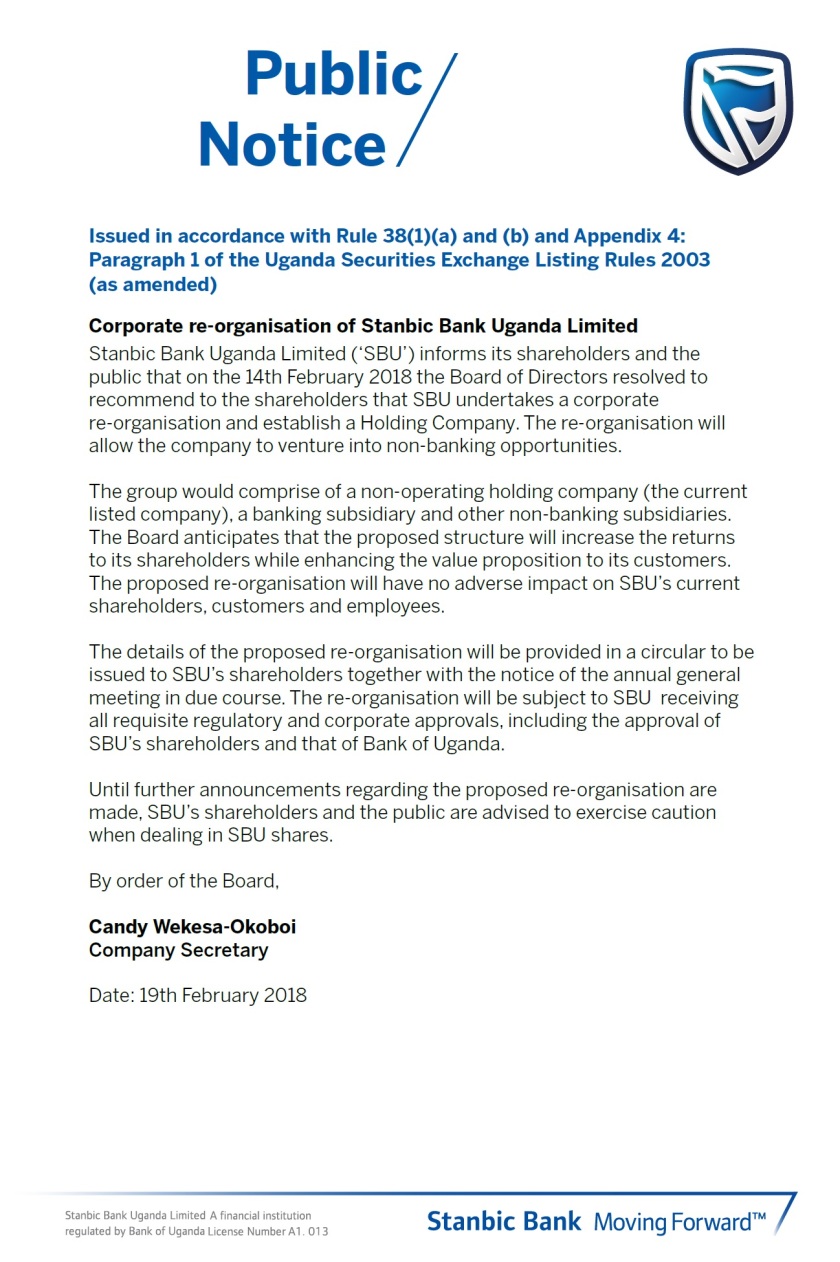

Stanbic Bank Uganda – Public Notice: “Corporate Re-Organization of Stanbic Bank Uganda Limited” (19.02.2018)

Share this:

Bank of Uganda report spells out growing non-performing loans and possible default of 9 banks!

Bank of Uganda’s late Annual Supervision Report of 2016 is finally out. Instead of mid-year, it was released in September. It must be reasons for that, since this is in the year two banks lost their balance and one was traded to another. The Crane Bank sale-off and losses have started most people, as also the expensive pens of the Bank. Therefore, with the procurement of pens must be the reason why the months from July to September to see the Annual report. The 2016 spreadsheet isn’t a fun read, it is dire and says something about the financial institutions, as well as the economy in general.

This report are telling stories of bad performing loans and the quality of them. When looking into that, you know that this is banking practice that supposed to be profitable. To loan money away that people save in the bank and gain interests. So, when the numbers are this crunching. When the state of affairs are so dire. When Government Securities and shortfall is what they are. Then you know there are failing prospects. As this the year after campaigns and elections. It is usually painful after the heavy spending and brown envelopes to anyone who support Mzee. That is why the costs and the non-performing loans are growing. But where that money went, is only known by the elite and the NRM. Take a look!

Non-Performing Loans:

“The analysis of default by the banks’ three largest borrowers and an increase in NPLs by 200 percent revealed large potential losses. It showed that if each bank’s three largest borrowers were to default, with a loan loss of 100 percent, 13 banks would become under-capitalised with an aggregate capital shortfall of USh.513.86 billion. If NPLs were to increase by 200 percent, assuming the increase is in the loss category which requires full provisioning, 9 banks would become under-capitalised with an aggregate capital shortfall of Ush.247.39 billion. A decrease in interest income from government securities would not require any additional capital from the banks” (BoU, P: 4-5, 2017).

Loan Quality:

“The banking sector’s overall asset quality continued to decline in 2016. The ratio of non–performing loans to total gross loans increased from 5.3 percent in December 2015 to 10.5 percent in December 2016. The increase in the NPL ratio was mainly on account of bad loans which more than doubled from USh.573.4 billion in December 2015 to USh.1,203.2 billion in December 2016” (BoU, P: 15, 2017)

Earnings and Profitability:

“There was a drop in profitability of the banking sector in 2016. Annual after tax profits reduced by 44.2 percent or USh.239.1 billion from Ush.541.2 billion in 2015 to USh.302.1 billion in 2016. Average return on total equity (ROE) dropped from 16.0 percent to 8.3 percent while return on assets (ROA) halved to 1.3 percent during that period. Total expenses grew by 9.3 percent, mostly in the form of interest expense on deposits. Increased provisioning for bad debts also reduced the banking sector’s earnings for the year under review. Provisions rose by more than 100 percent, by USh.419.4 billion to reach USh.637.2 billion in 2016” (BoU, P: 16, 2017).

So this growth isn’t making the economy more healthy. It is more bad loans and losses of profits. The bankers are not benefit ting and the costumers will pay for the shortfall in the long run. The assets and the basic needs will not be covered. The dangerous levels of NPL can even kill of more banks. As the reports not spelling out the names, but saying 9 banks could be under-capitalised, that means the government has to come in with security to put the bank on its feet or trade it off. Like it did with the Crane Bank recently.

Therefore, there are warning signs of continuing to borrow without security for repayment on the debt. That gives way for non-performing loans. This is the whole idea and reason for the problems the 9 banks have. As the costumers and corporations borrowing funds, without capacity to repay. That means the planned interest, the planned profits and repaid funds disappear. So, the more borrowed funds to try to catch the losses, is creating a evil spiral of losses. Instead of generating the profits and interests as anticipated.

Clearly, the banking sector needs a revamp and the system needs a push to make sure they are run smooth. As the consequence of continuing like nothing, is that further banks will default and costumers will lose savings and the state has to cough-up funds to save the scraps of a bank. Peace.

Reference:

Bank of Uganda – ‘ANNUAL SUPERVISION REPORT’ (December 2016) Volume 7 (06.09.2017)

Share this:

Opinion: Bank of Uganda must have bought magical pens!

Hey, Bank of Uganda, the glorious BoU, if you ever need any sort office equipment. I can sell it to you and at lesser cost. It will be fraction of the 357,000 Uganda Shillings per Pens or 125m shillings for 350 pens. At the dollar-rate, you paid $105 United States Dollar for each pen, they must be magnificent and the best pens ever made for the mankind.

Bank of Uganda, I understand the scrutiny you are under and as people are mocking this transaction, how you suddenly needed these expensive pens. I am sure they write the perfect lines and makes the others look like broke-back understudies without proper ink. The pens you bought must be most genuine Parker Pens, which brings the words so flawlessly on paper. When these pens touch the paper, they make such romance, so the ink flowers the paper and even smells better.

I have a feeling that the providers of these pen engraved them too each of the employees, so they have unique pen with their initials or even their nicknames. Therefore, they are all feeling unique and look well after.

“According to BOU, #BOUPens were “Cross” branded and meant to be sold as was the case with commemorative coins and notes in previous years” (NTV Uganda, 15.08.2017). So they were special and unique, they were designed in a way to make them feel special. Still someone who procured them really made a decent profit of the trade. Since pens usually doesn’t cost that much, even when your initially making them special too.

I am sure they bring back the good old times, sprint the words of Milton Obote and Idi Amin, even bring back Yusuf Lule, if lucky the grandest project of the all, the marvelous escape of the NRA. Certainly, the pens of the BoU must possess some sort of special powers. Since, they cost so much. All the things the pens has of value, so they can be used as collateral and even be pawned like jewels. Since they have such value and estimated cost.

So please Bank of Uganda, I got pens that can write in thin-air, spill the ink on the paper and give you the smell of roses. They will cost half of what you used to buy the Cross Pens, and they will look amazing. They will bring joy and happiness, maybe even be more within reason of cost. Since all paperwork and paper-trial of your clients, will smell like a bed of roses? It must be a dream and a dream worth living for, that you want to achieve in your lifetime.

Certainly, Bank of Uganda should consider some reasonable pens for their enterprise, as a state institution, but they are the ones keeping the inflation and the monetary policies at bay. Therefore, they need to be rewarded, not all can get Presidential Handshakes. Some just have to get pens, which are more valued than other people’s rents. That is their dumb luck, not the cashier at BoU. Peace.

Share this:

A look into ‘Project Nyonyi’ the PwC Forensic Review of the Crane Bank!

This are just one of them days, when the glaciers really get to much heat and becomes water. Than underneath all those years of ice and snow, you will find some relics of the past, which was hidden by the massive amounts of snow. That nothing these things hidden inside the glacier, that had the need to resurface, because no one would have the capacity to dig that deep. In the same sense, the PriceWaterhouseCoopers report of the Crane Bank reveal damaging reports on the state of the Bank. The Bank that Bank of Uganda took into receivership before trading to another third party. The bank that were praised and suddenly disgraced itself. Therefore, lets look at the important quotes from the report!

“This report has been prepared solely for BoU for use in considering immediate steps to safeguard Crane Bank’s interests and the additional investigative and evidence collation work that is required on key areas of concern to enable the preparation of a report that can be adduced as evidence in a court of law” (PwC, P:3, 2016).

“The above direct and circumstantial evidence suggests that Dr Ruparelia and persons associated with him, effectively owned and controlled 96% of CBL (With control of White Sapphire, the only shareholding not held by Dr Ruparelia and his immediate family, is the 4% shareholding held by Mr Jitendra Sanghani, (“Mr Sanghani”)). This contravenes the prohibition on an individual or body corporate controlled by one individual owning more than forty nine per cent of the Bank’s shares, and the restriction on the right to control financial institutions by those who are not reputable financial institutions or public companies as set out in S.18, and 24 of the Financial Institutions Act 2004 as amended (“FIA”)” (PwC, P: 14, 2016).

“The false accounting was partly achieved by crediting income with entries from off-book accrued interest receivables accounts and by keeping some liabilities (fixed deposits and borrowings from other financial institutions) off the books” (PwC, P: 15, 2016).

“The off book liabilities were brought back into the books in 2013 and a fictitious asset recognised by overstating the balances in the Nostro Account. It is not clear why CBL brought back this liability at this point. Due to this entry in the Nostro Account, as at 31 December 2013, there was a difference of USD 80m or UGX 200B between the system and actual balance in one of the Nostro Accounts; the Deutsche Bank USD account” (PwC, P: 15, 2016).

“As at 20 October 2016, loans amounting to UGX 63.6B had been advanced to related companies out of which lending totalling to UGX 63.1B (99%) had not been disclosed as insider lending. In addition to the companies considered as insiders in deriving the amount above, there are allegations that Logic Real Estates and Developers Limited (“Logic”) which had an outstanding balance of UGX 26.9 B as at 20 October 2016, is also related to Dr Ruparelia. Logic obtained this loan on 23 December 2014 and the amount appears to have been deposited back into a CBL “interest receivable” account labelled “Personal FD”” (PwC, P: 18, 2016).

It is not strange that a Crane Bank fell, when all the irregularities and mismanagement in their practices comes to the forefront. The Bank of Uganda could have seen this, but did not act upon it. They just let it be and let it go. That must have been because of the ties between Dr. Ruparelia and President Museveni. Certainly, the political affiliation has helped the financer and foreign investor in his prospects in Uganda. Since the off-books practices plus over-extended ownership did not apply to current legislation concerning healthy bank practices. Still, they let it all happen. This secret PwC report even entails provisions and statutes the owner of the bank has breached in his practices.

“Dr Sudhir Ruparelia: As a Director, major shareholder, vice chairman and generally as a person that exerted the greatest control over the Bank, Dr Ruparelia, concealed his true shareholding in the Bank; he oversaw the irregular transfer of the Bank’s branches to MIL, he benefitted from irregularly declared dividends, ‘due’ to White Sapphire; he conspired with others to embezzle/cause financial loss to CBL by use of cash extractions from Interdico, AI and TA; he was instrumental in the approval of credit facilities for related companies and associates, when there was no intention the loans would be repaid; and he failed to disclose his interests.

In addition to the above charges:

Receiving stolen property in respect of bank branch transfers, and White Sapphire dividends.

Embezzlement.

Influence peddling.

Nepotism.

Receiving and possessing property for himself or related parties, otherwise than in payment for the full value, in respect of the branch transfers, (FIA S126 (6).

Breach of the Prohibition on insider transactions” (PwC, P: 23, 2016).

When you read that a review and outsider opinion sees this and that the Bank of Uganda are just taken the bank into custody before trading it off to DFCU. Proves that they knew of the liabilities and the off-books practices, but put a blind an eye to the matter. Don’t see and don’t tell policy are clearly the BoU acts of the day, no matter what principle or legislation that has been breached by the former foreign investor in the good graces of the President.

Certainly, this is again, with all the other reports of the sudden fall of grace for the ones astonishing bank, the Crane Bank are now history and eaten by DFCU. While the subjects running this one to the ground are walking around like free men. The ownership and board are left off the hook, even as this secret report entail embezzlement and fraud of the bank. This is accepted and repeated without any consideration of all the clients and customers who at one point trusted the Crane Bank. They we’re used as pawns, to secure wealth for Dr. Ruparelia and his comrades. Peace.

Reference:

PriceWaterhouseCoopers (PWC) – ‘Project Nyonyi – Report on the Preliminary Forensic Review at Crane Bank’ (21.12.2016)

Share this:

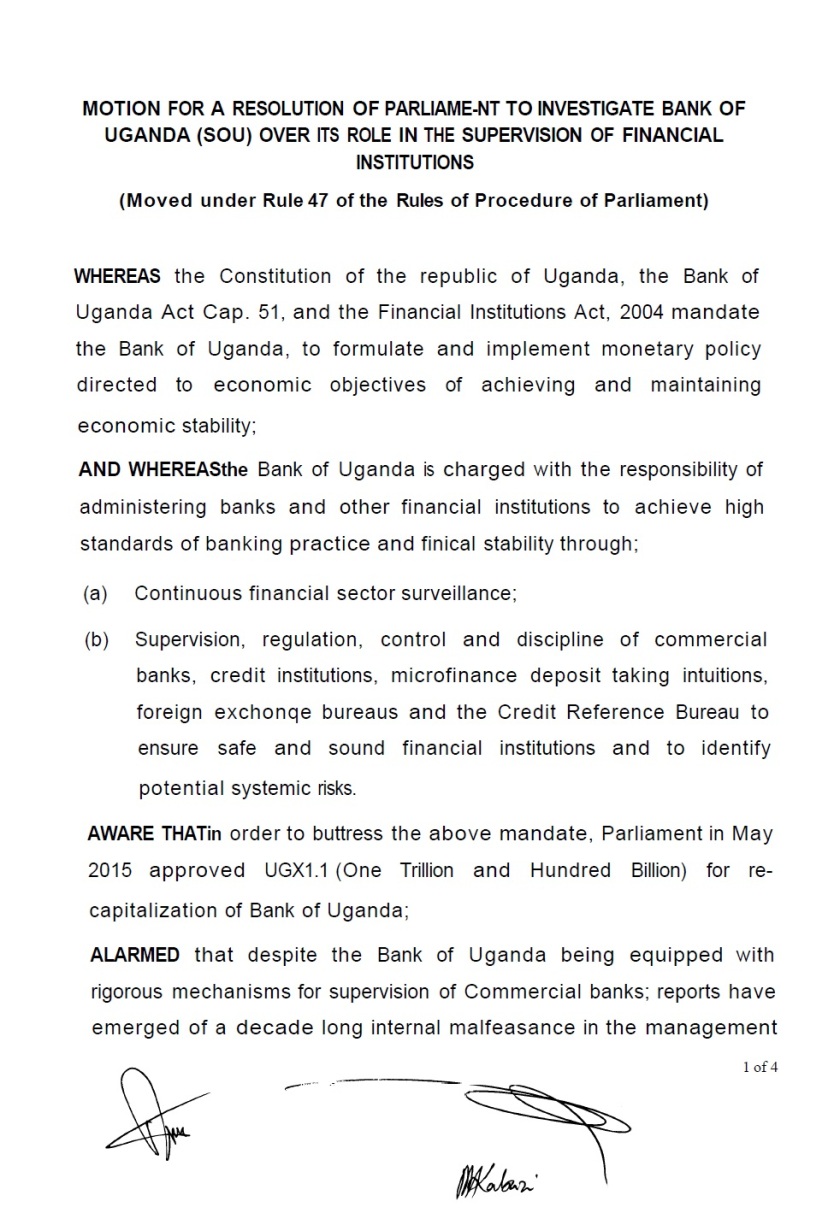

Motion for a Resolution of Parliament to Investigate Bank of Uganda (BoU) Over its role in the Supervision of Financial Institution (27.07.2017)

Share this:

Correction of factual Inaccuracies by The Observer News Paper concerning Ernst & Young (EY) as the auditors of Crane Bank (17.07.2017)

Share this:

Bank of Uganda: Resolution of Crane Bank Limited (13.07.2017)

Share this:

Derrick Nsereko issues notice of intention to sue BOU for not pursuiting the possible Crane Bank fraud case (12.07.2017)