Tag: Non-Performing Loans

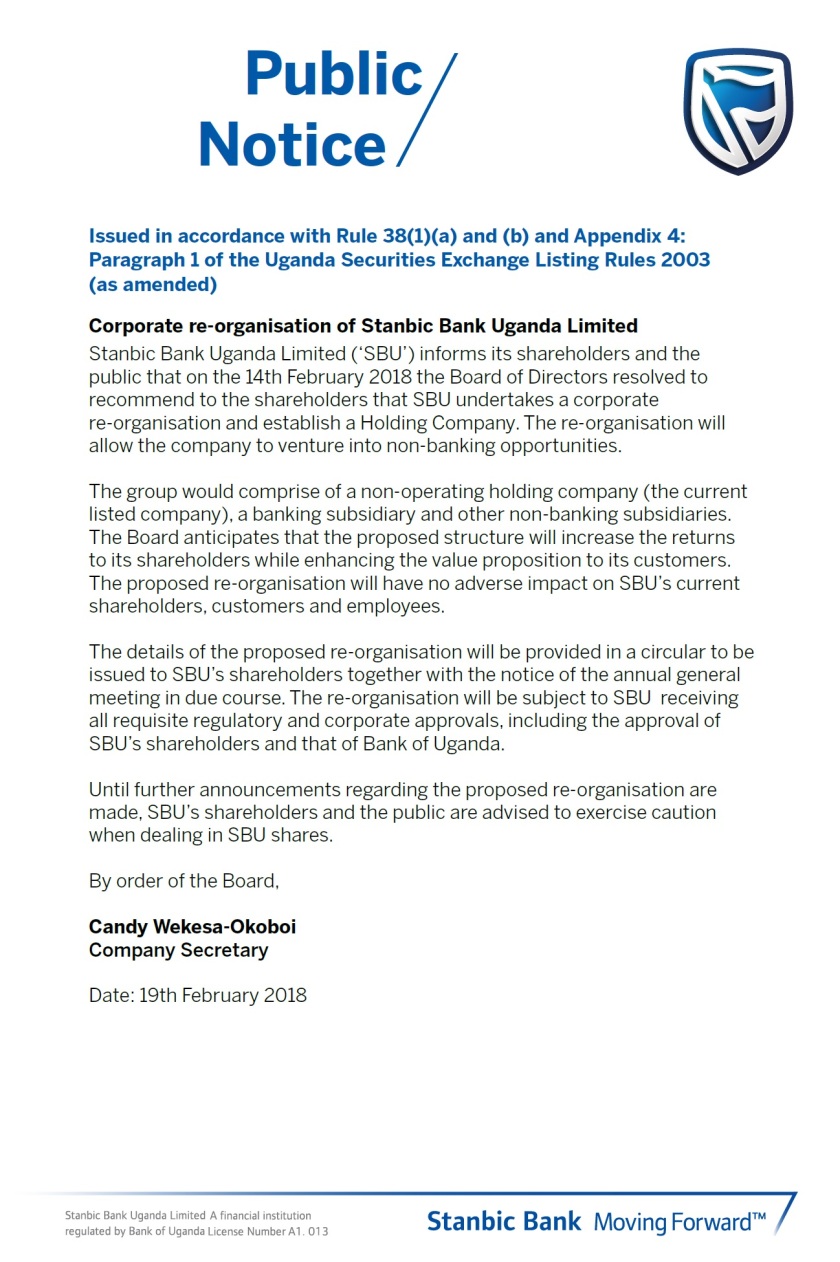

Stanbic Bank Uganda – Public Notice: “Corporate Re-Organization of Stanbic Bank Uganda Limited” (19.02.2018)

Share this:

Bank of Uganda report spells out growing non-performing loans and possible default of 9 banks!

Bank of Uganda’s late Annual Supervision Report of 2016 is finally out. Instead of mid-year, it was released in September. It must be reasons for that, since this is in the year two banks lost their balance and one was traded to another. The Crane Bank sale-off and losses have started most people, as also the expensive pens of the Bank. Therefore, with the procurement of pens must be the reason why the months from July to September to see the Annual report. The 2016 spreadsheet isn’t a fun read, it is dire and says something about the financial institutions, as well as the economy in general.

This report are telling stories of bad performing loans and the quality of them. When looking into that, you know that this is banking practice that supposed to be profitable. To loan money away that people save in the bank and gain interests. So, when the numbers are this crunching. When the state of affairs are so dire. When Government Securities and shortfall is what they are. Then you know there are failing prospects. As this the year after campaigns and elections. It is usually painful after the heavy spending and brown envelopes to anyone who support Mzee. That is why the costs and the non-performing loans are growing. But where that money went, is only known by the elite and the NRM. Take a look!

Non-Performing Loans:

“The analysis of default by the banks’ three largest borrowers and an increase in NPLs by 200 percent revealed large potential losses. It showed that if each bank’s three largest borrowers were to default, with a loan loss of 100 percent, 13 banks would become under-capitalised with an aggregate capital shortfall of USh.513.86 billion. If NPLs were to increase by 200 percent, assuming the increase is in the loss category which requires full provisioning, 9 banks would become under-capitalised with an aggregate capital shortfall of Ush.247.39 billion. A decrease in interest income from government securities would not require any additional capital from the banks” (BoU, P: 4-5, 2017).

Loan Quality:

“The banking sector’s overall asset quality continued to decline in 2016. The ratio of non–performing loans to total gross loans increased from 5.3 percent in December 2015 to 10.5 percent in December 2016. The increase in the NPL ratio was mainly on account of bad loans which more than doubled from USh.573.4 billion in December 2015 to USh.1,203.2 billion in December 2016” (BoU, P: 15, 2017)

Earnings and Profitability:

“There was a drop in profitability of the banking sector in 2016. Annual after tax profits reduced by 44.2 percent or USh.239.1 billion from Ush.541.2 billion in 2015 to USh.302.1 billion in 2016. Average return on total equity (ROE) dropped from 16.0 percent to 8.3 percent while return on assets (ROA) halved to 1.3 percent during that period. Total expenses grew by 9.3 percent, mostly in the form of interest expense on deposits. Increased provisioning for bad debts also reduced the banking sector’s earnings for the year under review. Provisions rose by more than 100 percent, by USh.419.4 billion to reach USh.637.2 billion in 2016” (BoU, P: 16, 2017).

So this growth isn’t making the economy more healthy. It is more bad loans and losses of profits. The bankers are not benefit ting and the costumers will pay for the shortfall in the long run. The assets and the basic needs will not be covered. The dangerous levels of NPL can even kill of more banks. As the reports not spelling out the names, but saying 9 banks could be under-capitalised, that means the government has to come in with security to put the bank on its feet or trade it off. Like it did with the Crane Bank recently.

Therefore, there are warning signs of continuing to borrow without security for repayment on the debt. That gives way for non-performing loans. This is the whole idea and reason for the problems the 9 banks have. As the costumers and corporations borrowing funds, without capacity to repay. That means the planned interest, the planned profits and repaid funds disappear. So, the more borrowed funds to try to catch the losses, is creating a evil spiral of losses. Instead of generating the profits and interests as anticipated.

Clearly, the banking sector needs a revamp and the system needs a push to make sure they are run smooth. As the consequence of continuing like nothing, is that further banks will default and costumers will lose savings and the state has to cough-up funds to save the scraps of a bank. Peace.

Reference:

Bank of Uganda – ‘ANNUAL SUPERVISION REPORT’ (December 2016) Volume 7 (06.09.2017)